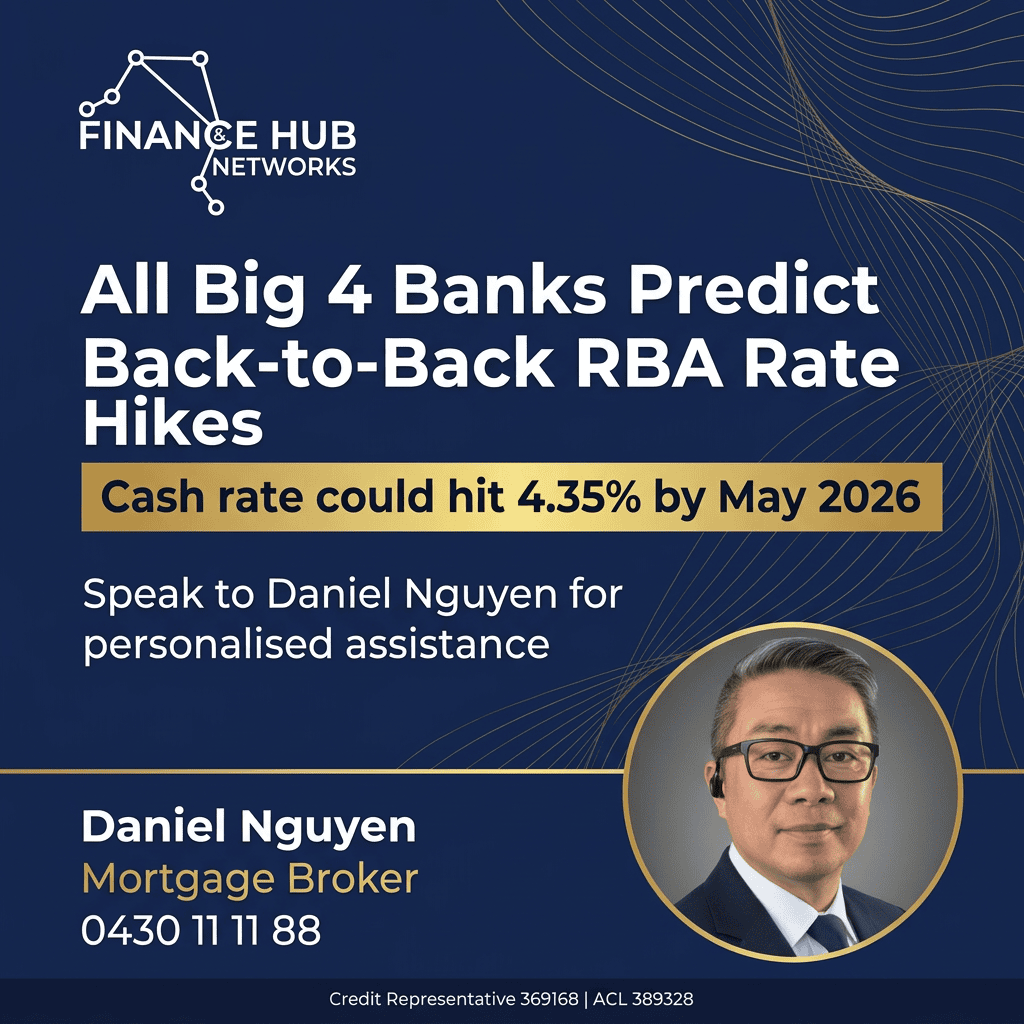

Australia’s mortgage holders are facing significant financial pressure as all four of Australia’s major banks — NAB, CBA, Westpac, and ANZ — have now aligned on forecasting back-to-back interest rate hikes from the Reserve Bank of Australia (RBA) in March and May 2026.

What Are the Big Banks Predicting?

As of March 2026, all Big Four banks have revised their cash rate forecasts upward. The consensus is clear:

- March 17, 2026 RBA meeting: All four major banks predict a 25 basis point rate hike, taking the cash rate from 3.85% to 4.10%

- May 2026 RBA meeting: A further 25 basis point hike predicted, taking the rate to 4.35%

- The bond market is pricing in approximately 68 basis points of additional hikes throughout 2026

Why Are Rates Rising Again?

Several factors are driving the shift in forecast:

- Sticky inflation: Australia’s January trimmed mean CPI accelerated to 3.4% year-on-year, above the RBA’s 2–3% target band

- Oil price shock: Rising global oil prices linked to Middle East tensions are fuelling inflationary pressures

- Demand-led inflation: Meals, clothing, and new dwelling costs all recorded stronger-than-expected rises in January 2026

- Reversal of 2025 cuts: The February 2026 hike and forthcoming increases would fully reverse the three rate cuts delivered in 2025

What This Means for Your Home Loan Repayments

If you have a $600,000 variable home loan, each 0.25% rate increase adds approximately $90–$95 per month to your repayments. Two hikes could increase your monthly repayments by nearly $180–$190.

For many households, this is the time to:

- Review your current interest rate — are you still on a competitive rate?

- Stress-test your budget at 4.35% to ensure you can manage higher repayments

- Consider fixing part of your loan to lock in certainty on a portion of your debt

- Refinance to a more competitive rate before further hikes take effect

- Speak with a mortgage broker who can compare options across multiple lenders

Should You Fix Your Rate Now?

With two predicted hikes on the horizon, many borrowers are weighing up whether to fix their rate. Fixed rates already reflect market expectations, so locking in now may not save money compared to variable — but it does provide repayment certainty during a volatile period. A mortgage broker can model the scenarios for your specific situation.

Act Now Before the Next RBA Meeting

The next RBA decision is on March 17, 2026. If you have been thinking about reviewing your home loan, now is the time to act — before any rate increase flows through to your repayments.

Need personalised assistance?

Contact Daniel Nguyen, Mortgage Broker at Finance Hub and Networks.

📞 0430 11 11 88

Credit Representative 573164 is authorised under Australian Credit Licence 573164. Your full financial situation would need to be reviewed prior to acceptance of any offer or product. Subject to lenders credit criteria, fees and charges will apply.