Trust borrowers face restrictive LVR caps, no LMI availability, trust deed certification costs, and lenders that won't count your real income. With 30+ lenders on our panel, we find the one that actually understands your trust structure — and says yes.

Trust borrowers face unique challenges that most lenders — and most brokers — simply don't understand.

"My accountant set up a family trust for asset protection, but now no lender will go above 80% LVR. I need a 20% deposit for a $1.2M property — that's $240,000!"

"I've been told I can't get Lenders Mortgage Insurance because the loan is in a trust name. Why does borrowing through a trust disqualify me from LMI?"

"The bank wants the trust deed certified by their panel solicitor at MY cost — on top of all the other legal fees. The certification alone costs $500–$1,500."

"My accountant distributes profits through the trust, but the lender only counts what's on my personal tax return. My trust earns $300K but I can only borrow based on $120K distribution."

"The bank declined my trust loan because it's a hybrid trust. I didn't even know there were trust types that lenders won't accept."

"Every director of my trustee company needs to personally guarantee the loan. My business partner doesn't want to be a guarantor — now what?"

Understanding how trusts work — and why lenders treat them differently — is the first step to getting approved.

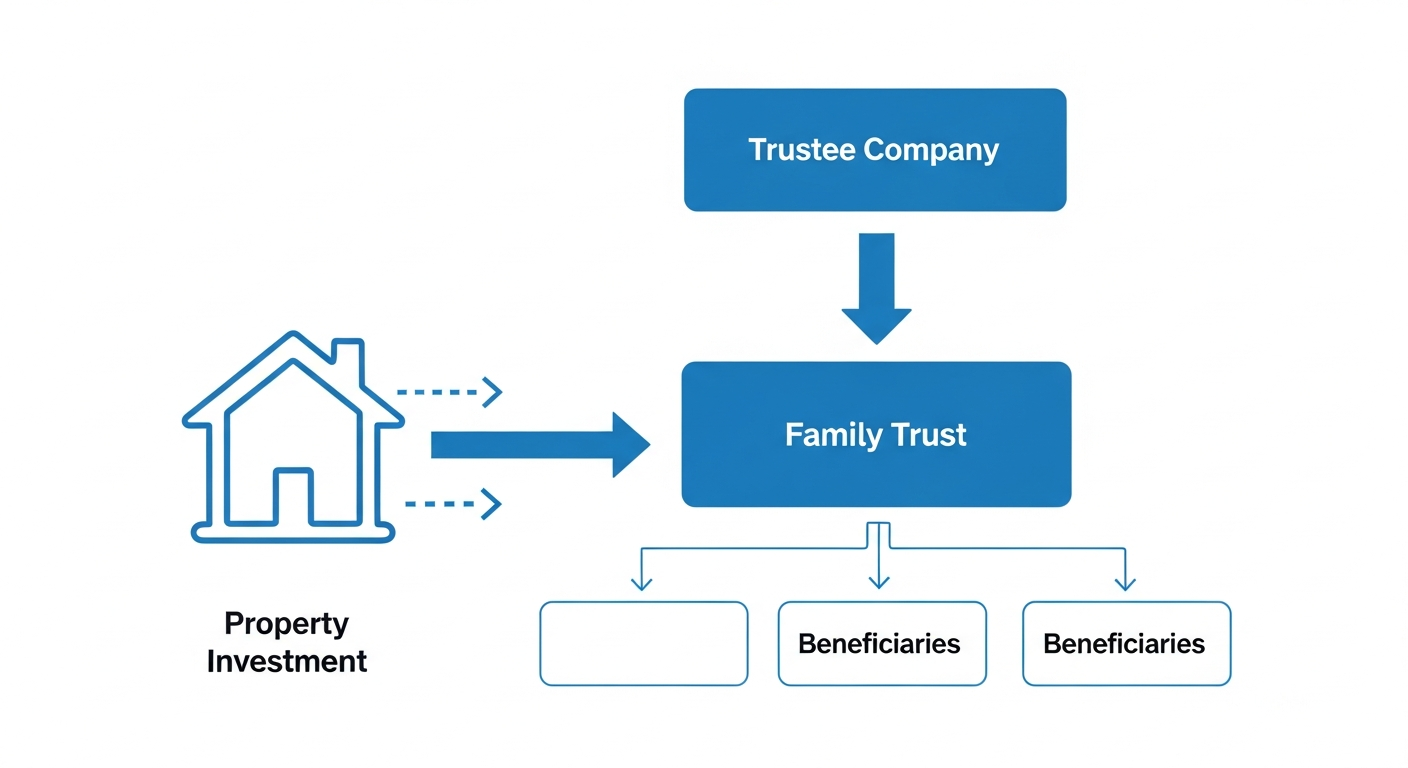

A trust is a legal arrangement where one party (the trustee) holds and manages assets on behalf of others (the beneficiaries). Unlike a company, a trust is not a separate legal entity — it's a relationship governed by a trust deed.

When you borrow through a trust, the trustee is the legal borrower and the registered owner of the property. But because the trust itself has no legal standing to sue or be sued, lenders require personal guarantees from the individuals behind the structure.

The most common trust type. The trustee has full discretion over how income and assets are distributed to beneficiaries. Accepted by most lenders.

Beneficiaries hold fixed units (like shares) with predetermined entitlements. Common for joint ventures and multiple investors. Accepted by many lenders.

A mix of discretionary and unit trust features. The combination of variable and fixed entitlements creates uncertainty. Most lenders reject hybrid trusts outright.

Only used for holding property on behalf of a Self-Managed Super Fund (SMSF). Not used for standard residential lending.

Created by a will and comes into effect after death. Generally not accepted for lending purposes.

Not all assessment methods are equal. The right approach can dramatically change your borrowing power.

Uses trust distributions shown on your individual tax return. The most common method for established trusts with consistent distribution history.

If you pay yourself a regular PAYG salary from the trustee company, some lenders will assess you like an employee — dramatically simplifying the process.

Comprehensive analysis of the trust's complete financial position. Takes more documentation but unlocks the highest borrowing power.

For trusts with irregular or difficult-to-document income, select non-bank lenders offer alternative documentation pathways.

Side-by-side comparison to help you identify the best path forward

| Feature | A: Distribution Income | B: Salaried Self-Employed | C: Full Financial | D: Alt Doc |

|---|---|---|---|---|

| Documentation Level | Moderate | Low | High | Low |

| Income Assessed | Trust distributions on personal return | PAYG salary from trust/company | Distributions + addbacks + undistributed profit | Self-declared / BAS |

| Max LVR | 80% | 80% | 80% | 70–80% |

| LMI Available | ✗ Generally No | ✗ Generally No | ✗ Generally No | ✗ No |

| Min Trading History | 2 years | 18 months | 2 years | 6–12 months |

| Borrowing Power | Moderate | Limited to salary | Highest | Moderate |

| Processing Speed | Standard | Faster | Slower | Standard |

| Lender Availability | Most major lenders | Select lenders | Most major lenders | Non-bank lenders |

| Ideal Candidate | Established trusts, consistent distributions | Directors on regular PAYG salary | Complex structures, max borrowing | New trusts, irregular income |

Trust lending involves specific requirements beyond standard home loans. Here's what you need to know.

Lenders require the trust deed to be reviewed and certified before approving the loan:

Because a trust has no legal personality of its own:

Trust loans face stricter lending thresholds:

Business registration and security agreements:

Not all trusts are treated equally by lenders:

Trust requirements vary by Australian state:

Every trust situation is unique. Here's how we've helped borrowers just like you get approved.

Get a quick estimate of your borrowing power, likely LVR cap, and what documents you'll need.

Answer a few quick questions to see your indicative borrowing position

⚠️ This is an indicative estimate only. Actual borrowing power depends on full financial assessment. Get a free personalised assessment →

We don't just process loans — we specialise in complex trust lending that other brokers can't handle.

We understand the nuances of discretionary trusts, unit trusts, hybrid trusts and company trustee structures — inside and out.

With 30+ lenders on our panel, we know exactly which lenders accept your specific trust type and structure — saving you weeks of rejections.

We manage the entire trust deed certification process, liaise with solicitors, and ensure your deed meets lender requirements before lodging.

We structure your application using the assessment method that gives you the highest borrowing capacity — not just the easiest to process.

Our service costs you nothing. The lender pays our commission when your loan settles. That's it.

Don't take our word for it — read what hundreds of trust borrowers and property investors say about working with us.

We make the complex simple. Here's how it works.

Tell us about your trust type, trustee structure, income, and property goals. We'll identify the best assessment pathway from day one.

Using our 30+ lender panel, we find the lender that accepts your trust type, offers a competitive rate, and maximises your borrowing power.

We handle the trust deed certification, manage the application end-to-end, and keep you informed at every stage until settlement.

Everything trust borrowers need to know about getting a home loan through a trust structure.

Tell us about your trust structure and we'll identify the best lender and assessment pathway — at no cost to you.

A trust lending specialist from Finance Hub will review your details and contact you within 2 business hours.

Prefer to speak with a trust lending specialist directly? Book a time that suits you.

📋 Explore More

We offer 25+ home loan and finance solutions for every situation, profession, and lending challenge.

Browse All Services →